This paper addresses a subtle but important assumption in the broad literature on stock price synchronicity, that is, whether the standard errors used in hypothesis testing are well defined. Findings of relationships between synchronicity and explanatory variables are often unstable or reverse their sign in subsequent research using a different time period. This paper offers a simple explanation for these contradictory findings. Research into stock price synchronicity has a kurtosis problem. As a consequence, results in research using R-squared as a dependent variable are suspect. Estimation of stock price synchronicity typically requires the kurtosis of underlying firm-specific returns to be finite, but a large proportion of stocks is likely to have infinite or undefined kurtosis, which invalidates estimates of synchronicity for these stocks. Therefore, stock price synchronicity cannot be known in general and may be estimated only if finiteness of kurtosis can be established.

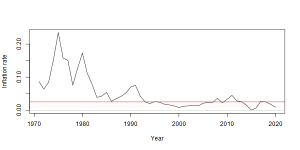

Estimating the value of an inflation-capped pension from market data

1 November 2021

The University Superannuation Scheme (USS) is planning to introduce a cap of 2.5% for inflation adjustments to its members’ accrued pensions. The effect of this cap is to increase new accrued pension benefits in line with official consumer prices (CPI) but only up to 2.5% per year. If inflation runs hotter than 2.5%, that year’s …

Continue reading